By

Brian Kinsley

Updated:

Listen to this article: Understanding Uninsured and Underinsured Motorist Coverage in Alabama — a narrated guide covering what happens if the other driver doesn’t have enough insurance. 13 minutes.

When the driver who caused your accident doesn’t carry enough insurance, your own policy may be the most important safety net you have. This article explains how uninsured (UM) and underinsured (UIM) motorist coverage works in Alabama, including what each one covers, how they fit alongside the state’s minimum liability limits of $25,000 per person and $50,000 per accident, and why those minimums often fall short after a serious wreck. It walks through how UM/UIM claims are filed against your own insurer, what you have to prove to recover, and how Alabama’s strict contributory negligence rule can affect your case even when you’re the one who was hurt. It also covers the settlement steps that matter most in UIM cases, including why you should never sign a release from the at-fault driver’s insurance company without first notifying your own UIM carrier. Along the way, it answers common questions about coverage limits, premiums, passengers, and the right time to review your policy, all aimed at helping Alabama drivers understand where they stand before an accident ever happens and what to do if one already has.

Most of us don’t spend much time thinking about the other drivers on the road. We assume they’re insured. We assume they carry enough coverage to make things right if something goes wrong. Then a serious accident happens, and one of the first hard questions becomes: “How much insurance does the other driver actually have?”

In Alabama, the answer matters more than most folks realize. Medical bills pile up fast. Out here in Cullman County, where so much of our daily driving happens on I-65, Highway 157, and the back roads in between, a serious wreck can upend a family’s finances overnight. Missed paychecks follow close behind. And when the driver who caused the wreck carries little or no insurance, the road to recovery can get steep in a hurry.

That is where uninsured and underinsured motorist coverage—usually called UM and UIM—comes in. It is the coverage you carry on your own policy to protect yourself and your family when the at-fault driver cannot. Think of it as a safety net you hope to never need, but are grateful for when you do.

Understanding how UM and UIM coverage works, both before a wreck and after one, can make a real difference in how your claim turns out.

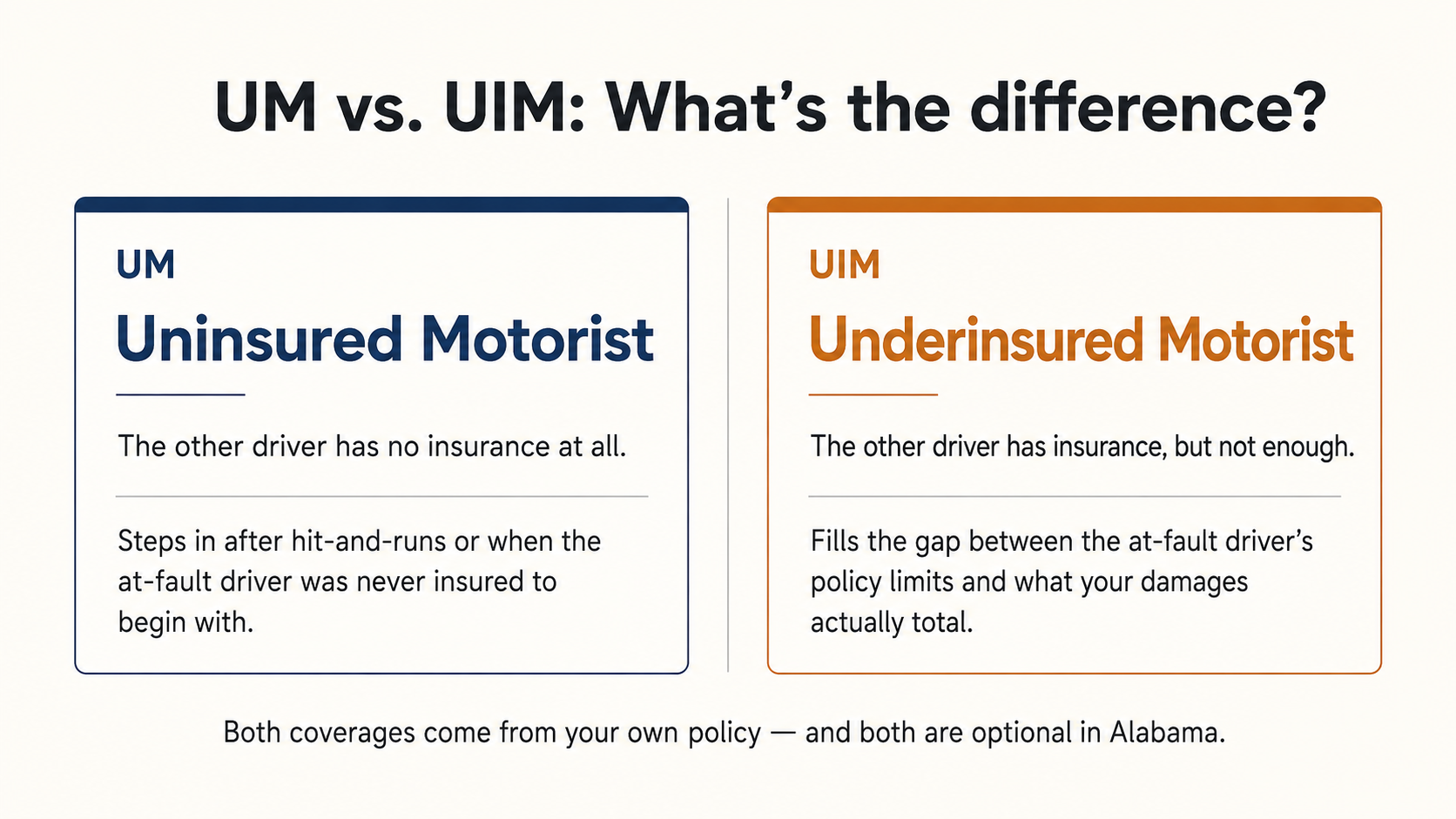

What Is Uninsured Motorist (UM) Coverage?

Uninsured motorist coverage, or UM, steps in when the at-fault driver has no liability insurance at all. Alabama law requires every driver to carry coverage, but the truth is, plenty of people on the road still do not. Some let their policies lapse. Others never bought a policy in the first place. Either way, if one of those drivers causes your accident, you are left holding the bill unless you have protection of your own.

UM coverage can also come into play after a hit-and-run, when the driver who caused the wreck takes off and cannot be identified. In those moments, your own policy becomes the one place you can turn.

When UM coverage applies, your insurance covers damages that the at-fault driver should pay. This protection includes medical costs, lost wages, and often pain and suffering, depending on your policy and case details. The purpose of UM coverage is to prevent an irresponsible or unidentified driver from leaving you to bear the costs of their mistake. Typically, UM/UIM coverage handles bodily injury damages, covering medical bills, missed paychecks, and pain and suffering, in accordance with your policy and Alabama law.

What Is Underinsured Motorist (UIM) Coverage?

Underinsured motorist coverage, or UIM, is built to fill the gap when the at-fault driver has insurance, but not nearly enough to cover the full weight of your damages.

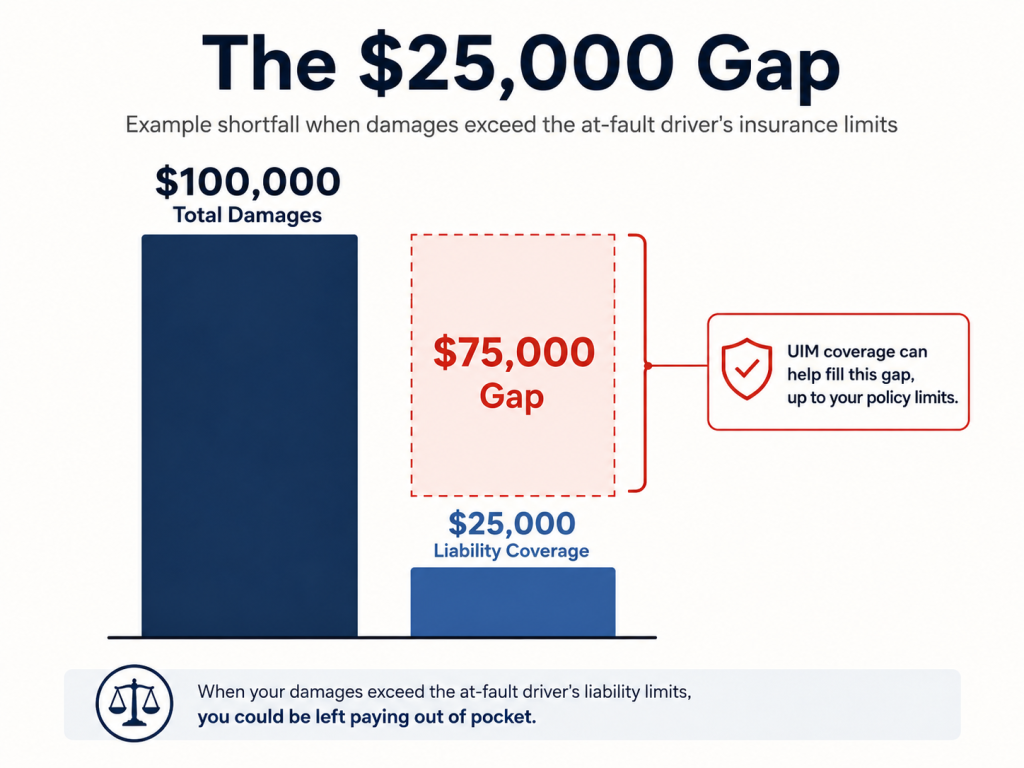

For example, say there’s a wreck on I-65 near the Cullman exit. Your damages total $100,000, but the at-fault driver only carries the state minimum of $25,000. That leaves a $75,000 shortfall, and without UIM coverage of your own, that gap becomes your problem to solve. UIM coverage is built to close that gap, up to the limits on your own policy — so a shortfall on the other driver’s side doesn’t automatically become yours.

Under Alabama law, underinsured motorist situations fall within the broader uninsured motorist framework. In other words, the statute treats “not enough insurance” as a form of “no insurance” once the at-fault driver’s limits have been exhausted. It is a small distinction on paper, but an important one in practice, because it is what allows your own UM/UIM coverage to step in and help close the gap.

Alabama’s Minimum Liability Requirements

Alabama law requires drivers to carry minimum liability insurance, currently $25,000 per person and $50,000 per accident for bodily injury, and $25,000 per accident for property damage.

Here is the hard truth about those numbers: they do not go very far. One trip to the emergency room, one surgery, one stretch of physical therapy — and you can exceed $25,000 before you can blink. Add in lost wages and other damages, and the gap between what the at-fault driver’s policy covers and what you actually need can be staggering. That is exactly the hole UM/UIM coverage is designed to fill.

Is UM/UIM Coverage Required in Alabama?

Not exactly, and this is where a lot of folks get tripped up. Alabama law requires every insurance company to offer uninsured motorist coverage when they sell you an auto policy. But you, as the policyholder, have the right to turn it down in writing.

That small piece of paperwork has big consequences. Many drivers sign their policies without ever realizing they waived the very coverage that could protect them down the road. Others simply are not sure what they have.

The best way to know where you stand is to pull out the declarations page of your policy. It lists your coverage types and your limits in black and white. Take a few minutes to look it over, and if anything is unclear, call your agent and ask. A short conversation today can spare you a world of worry later on. If your declarations page does not show UM/UIM coverage, do not assume either way; ask your agent or insurer for confirmation and a copy of any rejection form in your file.

How UM/UIM Claims Work

Unlike a typical liability claim, a UM/UIM claim is filed against your own insurance company rather than the other driver’s, but do not assume that makes recovery automatic.

Your own insurance company still has the right to evaluate the claim from top to bottom, weighing fault, damages, and the documentation behind them. In practice, a UM/UIM claim often looks a lot like a traditional personal injury case, with the same scrutiny and the same need for careful presentation.

To recover under UM or UIM coverage, you generally must prove:

- The other driver was legally at fault

- You suffered compensable damages

- The at-fault driver was uninsured or underinsured

Once established, your insurer may be required to compensate you up to your policy limits.

Alabama’s Contributory Negligence Rule

Alabama adheres to a strict contributory negligence standard. Under this rule, if the injured party is found even slightly at fault—even just 1%—it can completely bar any recovery on a negligence claim. While there are certain exceptions, such as cases involving wantonness or willful conduct, this high bar is the reason why establishing the other driver’s clear fault is so critical to your case.

This rule applies to Underinsured Motorist (UM) and Uninsured Motorist (UIM) claims. Even when you are filing against your own insurer, the other driver’s fault still has to be established clearly. Getting photos of the scene, seeking medical care right away, and collecting witness information are not just good habits — in Alabama, they can be the difference between a recovery and a dead end.

Schedule a

Free Consultation

Settlement Considerations in UIM Cases

UIM claims involve two insurance companies at once — the at-fault driver’s carrier and your own. The order of operations matters, and small missteps can cost you coverage you’ve already paid for.

Before accepting a settlement from the at-fault driver’s insurance, it’s important to follow specific procedures. Signing a release improperly can risk your right to seek additional compensation under UIM coverage.

- Notify your own UIM carrier as soon as a shortfall looks likely

- Do not sign any release from the at-fault driver’s insurer without approval

- Give your UIM carrier the chance to advance the settlement amount and protect its rights

- Do not finalize a settlement or sign a release until you have complied with your policy and Alabama’s UIM settlement-notice requirements

This is where having a lawyer involved early pays off — before a well-meaning signature costs you thousands

Common UM/UIM Scenarios in Alabama

We’ve sat across the table from more than one family right here in Cullman who walked in assuming the other driver’s insurance would cover everything — and learned the hard way that the at-fault driver had the $25,000 minimum and no assets behind it. UM/UIM coverage often applies in situations such as:

- Drivers carrying only minimum liability coverage causing serious injuries

- Hit-and-run accidents where the at-fault driver cannot be identified

- Commercial vehicles with insufficient policy limits

- Multiple victims exhausting available liability coverage

In these cases, UM/UIM coverage can be an important source of recovery.

Frequently Asked Questions About Uninsured and Underinsured Motorists

Most folks have the same handful of questions when they first call us about an uninsured or underinsured driver. Here are the ones that come up most often, and the answers we give.

Answer: Yes. UM/UIM claims may proceed in a manner similar to litigation, depending on the policy and case circumstances.

Answer: It depends on the insurer and the facts of the claim. These coverages exist specifically to protect you when another driver cannot pay.

Answer: Your declarations page lists your UM/UIM coverage. Many policyholders are surprised to learn their limits are lower than expected.

Answer: In many cases, passengers in your vehicle may also be covered under your policy, but it depends on the policy definition of an insured and the circumstances of the crash.

Why Early Coverage Review Matters

The best time to review your insurance coverage is at the start of a claim, not weeks later during negotiations. Early reviews clarify important details, like the at-fault driver’s liability coverage and your own uninsured (UM) and underinsured (UIM) motorist coverage. It also highlights any policy rules or deadlines that could impact your case strategy.

Protecting Yourself Before an Accident

UM/UIM coverage becomes critical after an accident, but the best time to look at it is long before one ever happens.

State minimum liability limits rarely come close to covering the real cost of a serious injury. Raising your UM/UIM limits is usually inexpensive, and the protection it provides can be the difference between recovery and financial hardship.

A quick policy review every year or so is one of the simplest ways to make sure you and your family are not left exposed when it matters most.

Free Case Evaluation

We’ll look at your policy with you, explain where you stand in plain English, and tell you honestly whether you need a lawyer or whether this is something you can handle on your own.

No pressure, no cost to talk. That’s just how we do things around here.

Disclaimer

This article is for informational purposes only and does not constitute legal advice. Reading this content does not create an attorney-client relationship. Every case must be evaluated based on its individual facts and circumstances.